6 min read

The Hidden Ops Cost Of Manual & Dual Entry International Wire Processing

Your International Wire Process Isn't Broken. It's Just Quietly Expensive. Ask most operations managers at a community...

If you had to sum up the goal of ISO 20022 in a single word, it is to “unify.” Transferring money across borders has long been a complex and slow process, hindered by a patchwork of rules and incompatible systems. ISO 20022 aims to change all that. This global international payments standard akin to a universal adapter enables all these disparate financial institutions, market infrastructures, and end-user communities to communicate with each other through one common language.

.png?width=600&height=300&name=ISO%2020022%20Header%20(1).png)

By standardizing how payment information is exchanged, ISO 20022 reduces errors, saves time, improves sanctions compliance, and enhances clarity — paving the way for a revolutionary shift in the speed, accuracy and reliability of international payments.

ISO 20022 adoption has been mandated globally, with major payment systems like SWIFT, the Federal Reserve’s Fedwire, and the Clearing House Interbank Payments System (CHIPS) transitioning to the new standard. The final deadline for full conversion to the new standard across SWIFT’s network is November 2025. Institutions that fail to adopt ISO 20022 risk operational disruptions and loss of competitiveness in the increasingly global and digital financial ecosystem.

Despite its benefits, many community financial institutions are struggling to keep pace with the November 2025 compliance deadline. According to a Finextra report fewer than 40% of banks in North America feel confident in their ability to meet the ISO 20022 requirements. Challenges include outdated infrastructure, a lack of technical expertise, and the perception that compliance is optional. However, community banks cannot afford to lag behind, as non-compliance can lead to operational disruptions, regulatory penalties, and even reputational damage. We spoke with Marcia Klingensmith, CEO of Fintech Consulting LLC, to explore practical strategies for implementing the standard and unlocking its full potential.

ISO 20022 is a global financial messaging standard designed to unify and streamline communication across payment systems worldwide. Created and maintained by the International Organization for Standardization (ISO), ISO 20022 was developed through collaboration among financial industry experts, including contributions from SWIFT, which serves as its registration authority. This standard introduces a single, consistent approach to structuring and handling international payment data, replacing fragmented and proprietary legacy systems.

“The true power of ISO 20022 — which I call the Financial Rosetta Stone — lies in its ability to support rich, structured, and machine-readable data, enabling interoperability between financial institutions, market infrastructures, and end-user systems,” Klingensmith says. She explains the value propositions further in this video:

“ISO 20022 standardization makes it easy to map the transaction data into accounts payable and accounts receivable (AP/AR) systems,” Klingensmith says. “This allows for automation of key tasks like invoice processing, reconciliation, and payment matching, significantly reducing manual effort and errors. Banks can leverage this to streamline their internal operations and create valuable products for their business customers.”

Imagine a service called ‘Automated Reconciliation powered by ISO 20022.’ This could extract data from ISO 20022 messages, map it to the customer's accounting software (like QuickBooks or SAP), and automatically reconcile payments with invoices. This saves businesses significant time and reduces errors, improving cash flow and efficiency. Banks could offer tiered services with varying levels of automation and integration, catering to businesses of all sizes. Further, by promoting ISO 20022 adoption, banks improve their own operational efficiency through standardized data exchange. This is a win-win scenario where banks enhance customer relationships, generate new revenue streams, and gain a competitive edge by offering innovative, value-added solutions.

It can also improve security and fraud detection: “It makes it a lot easier to triangulate and detect patterns when you’ve got a standardized language,” Klingensmith says, adding that smaller institutions have much to gain through these advancements.

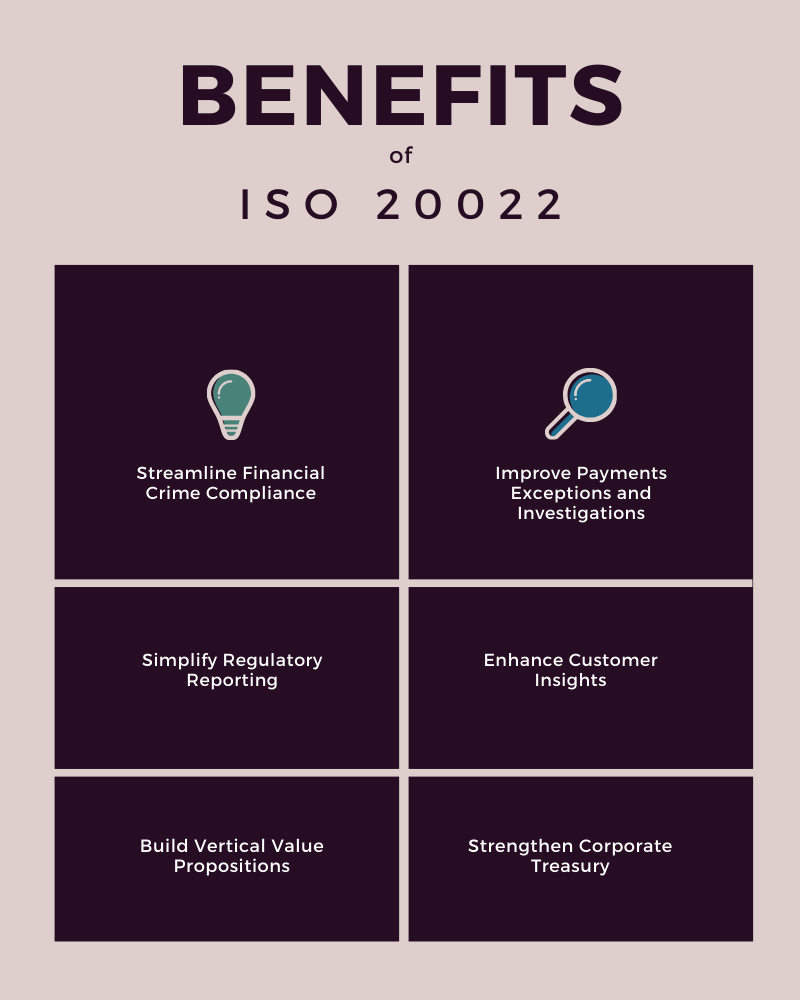

1. Streamline financial crime compliance

Challenge: Unstructured data in legacy systems often blends key details like names and addresses into the same field, triggering false alerts and increasing manual investigations.

Opportunity: ISO 20022 uses structured data, such as dedicated fields and entity identifiers, to reduce false positives and streamline anti-money laundering (AML) sanctions screening. This improves efficiency, lowers costs, and allows teams to focus on real risks.

2. Improve payments exceptions and investigations

Challenge: Incomplete or missing payment details cause 2-5% of transactions to require manual investigation, delaying resolution and increasing costs. Unique regulatory requirements also add complexity.

Opportunity: ISO 20022 enables richer data capture and standardized tagging to reduce exceptions and prioritize investigations. Enabling up to 84% of messages to be automatically sorted by investigation type streamlines processes and speeds up resolution time.

3. Simplify regulatory reporting

Challenge: Missing or misinterpreted data in free-text fields makes regulatory reporting time-consuming and prone to errors, especially for country-specific requirements.

Opportunity: ISO 20022’s standardized data fields ensure accurate, automated reporting. This reduces manual intervention, simplifies compliance, and improves overall efficiency while lowering operational costs.

4. Enhance customer insights

Challenge: Non-standardized formats make it difficult to analyze customer behavior and identify their needs. Truncated or inconsistent remittance data adds complexity, slowing resolution and decision-making.

Opportunity: ISO 20022’s structured data allows banks to understand who customers transact with and why, unlocking opportunities to offer tailored products. For example, identifying tuition payments could trigger campaigns for student loans or financial planning services. By linking transactions to reference data like invoice numbers or customer IDs, banks can gain deeper insights to improve service and drive growth.

5. Build vertical value propositions

Challenge: Creating new products and capabilities to retain market share is difficult without a clear view of customer payment needs. Inconsistent use of ISO 20022 in corporate payments adds friction, delaying resolution and impacting supplier operations.

Opportunity: ISO 20022 unlocks the ability to offer innovative services tailored to specific customer needs. For instance, smart invoice financing leverages payment data and industry insights to validate invoice legitimacy, analyze payment histories, and determine optimal financing terms. This enables banks to provide faster and more reliable funding options to businesses.

The enriched, structured data of ISO 20022 also facilitates automated reconciliation for high-volume payment companies and enhances straight-through processing by identifying recurring errors and helping customers correct initiation data. Additionally, ISO 20022 supports emerging payment services like Request to Pay and Payment Initiation Services, offering businesses greater flexibility and efficiency.

6. Strengthen corporate treasury

Challenge: Treasury teams face delays from incomplete or truncated data, inconsistent messaging formats, and reliance on manual intervention. These issues hinder cash flow analysis, disrupt forecasting, and slow payment investigations, often delaying supplier production cycles. Inconsistent use of ISO 20022 in corporate payments over SWIFT further complicates processes.

Opportunity: ISO 20022 provides real-time visibility into cash flows with structured data that reduces manual intervention and accelerates reconciliation. This improves cash forecasting, liquidity management, and financial efficiency. Businesses can release goods faster, optimize working capital, and streamline treasury operations.

Additionally, ISO 20022 supports advanced services like “On Behalf Of” (OBO) payments, enabling easy identification of initiating and ultimate debtor/creditor parties, and simplifying virtual account management.

ISO 20022 isn’t just about meeting compliance deadlines — it’s also a powerful tool for unlocking new revenue streams. The rich, structured data that comes with this standard opens the door for banks to offer value-added services and deepen customer relationships while driving profitability.

The enriched data provided by ISO 20022 enables banks to deliver personalized insights through detailed transaction reports and analytics. For example, banks can categorize a customer’s spending patterns, helping them forecast budgets or identify inefficiencies in their cash flow. These insights create opportunities for premium, fee-based services, such as subscription analytics tools or customized financial health reports. Customers benefit from greater financial clarity, while banks strengthen engagement and boost new non-interest income generation.

Klingensmith explains: "With ISO 20022, you can have special message fields to capture what the transaction’s about. You can start learning your customers’ patterns of payments, and you can start offering new products based on those insights."

With ISO 20022, banks gain a clearer view of customer behavior through transaction patterns. By analyzing this data, banks can identify specific customer needs and proactively recommend relevant products or services. For instance, a business making regular large purchases could be presented with an overdraft facility or business line of credit. This approach not only generates revenue but also increases customer satisfaction by addressing their unique financial needs.

Banks can offer tailored B2B services, such as automated reconciliation tools or enhanced reporting capabilities, which streamline financial workflows for their clients. By providing these high-value services, banks position themselves as indispensable partners in the financial supply chain, further reinforcing long-term relationships and capturing additional revenue opportunities.

Klingensmith talks more about the potential for personalization that ISO 20022 presents:

ISO 20022 can be likened to a universal adapter for financial messaging, helping to bridge the fragmented system of legacy formats — akin to how a universal power adapter connects devices with different plug types.

ISO 20022 messages can be expressed in multiple formats — such as XML or ASN.1 — making them highly adaptable to different systems and workflows. Additionally, its structured approach facilitates interoperability with other financial standards, like FIX and FpML, in broader financial ecosystems. This flexibility allows financial institutions to integrate ISO 20022 into their existing operations without relying on outdated technologies, while also preparing them to adopt future innovations like advanced analytics and artificial intelligence (AI) with minimal disruption.

The real power of ISO 20022 lies in its ability to handle far more data in a clear and organized manner. It’s like upgrading from an outdated, hard-to-read format to a streamlined system where every field has a precise purpose — whether it’s the transaction amount, purpose of payment, or recipient details. Banks can leverage this wealth of data to enhance critical processes, such as sanctions screening, fraud detection, and customer analytics.

If ISO 20022 is a standardized blueprint for organizing and exchanging financial data, then XML (eXtensible Markup Language) is the vehicle that transports this structured data efficiently. XML is a syntax that organizes and structures ISO 20022 data using tags. These tags define the format, structure, and meaning of the data, enabling seamless information exchange across platforms.

In global payments, XML ensures consistency and adaptability, supporting local regulations and evolving standards. For example, XML messages can include:

Tax details for transactions

Comprehensive transaction descriptions

Information about intermediaries in the payment chain

This standardization is critical for creating efficient and harmonized payment processes worldwide.

Traditionally, financial institutions relied on the SWIFT MT messaging format to send international wires, which uses a limited text structure. In contrast, ISO 20022 introduces the MX format, which enables standardized, detailed, and structured payment data across global financial systems.

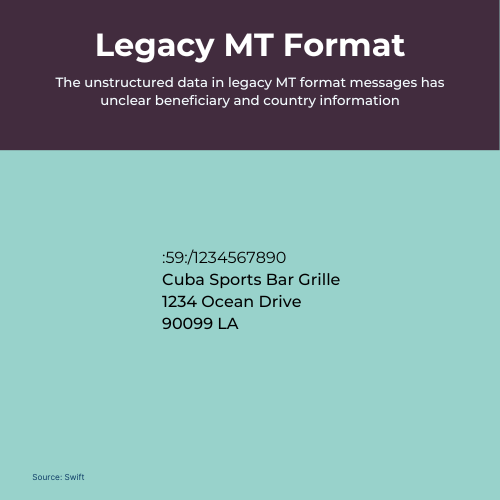

Many existing systems rely on free-text address fields, where name and address information are entered as open lines with character limits. In this legacy format, key details can appear anywhere within the lines, leading to inconsistencies.

For example, here’s how a wire instruction might look in the legacy MT format:

In the legacy MT format example, there’s no clear distinction between the business name, address, and country of origin. A payment referencing “Cuba Sports Bar & Grille” would likely be flagged by a sanctions filter due to the word “Cuba” appearing in the name and address. Without a clear structure, it’s difficult to determine whether “Cuba” refers to the business name or the country, leading to a false positive and triggering a manual investigation.

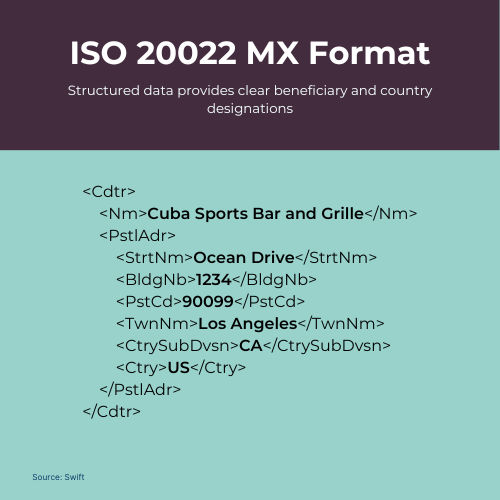

In contrast, ISO 20022 messages use XML tags to organize details into clearly defined fields, specifying the start and end of each element. The Postal Address field explicitly identifies the country of the business — <Ctry> US /Ctry> — using a standardized 2-character country code. Additionally, the Name field <Nm> field confirms that “Cuba” is part of the business name, not the country. This clarity prevents false compliance hits, allowing the payment to process smoothly, reducing manual intervention costs, and ensuring the funds arrive on time.

Additionally, there are separate identifiers for each address component, such as street name, building number, state, country, and even specific departments within an organization. This more structured format eliminates ambiguity, making it easier for systems to accurately process and identify address details.

The standardized ISO 20022 format also enables banks to capture other key data, such as the Postcode (PstCd), which can be used for compliance checks and demographic analysis. With enhanced clarity of all transaction data, banks can better manage risks, understand where payments originate and terminate, and improve wire processing efficiency across the entire payments process.

|

Field |

Tag |

Character Limit |

|

Address Type |

<AdrTp> |

(4 characters) |

|

Department |

<Dept> |

(up to 70 characters) |

|

Sub Department |

<SubDept> |

(up to 70 characters) |

|

Street Name |

<StrtNm> |

(up to 70 characters) |

|

Building Number |

<BldgNb> |

(up to 16 characters) |

|

Building Name |

<BldgNm> |

(up to 35 characters) |

|

Floor |

<Flr> |

(up to 70 characters) |

|

Post Box |

<PstBx> |

(up to 16 characters) |

|

Room |

<Room> |

(up to 70 characters) |

|

Post Code |

<PstCd> |

(up to 16 characters) |

|

Town Name |

<TwnNm> |

(up to 35 characters) |

|

Town Location Name |

<TwnLctnNm> |

(up to 35 characters) |

|

District Name |

<DstrctNm> |

(up to 35 characters) |

|

Country Sub Division |

<CtrySubDvsn> |

(up to 35 characters) |

|

Country |

<Ctry> |

(2 characters) |

Access the full list of ISO 20022 XML Tag abbreviations.

ISO 20022 XML files are structured into three primary sections, each serving a specific purpose:

1. Group header

Provides an overview of the entire file, including key details such as the message reference, creation date and time, grouping type, total number of transactions, and sender identification.

2. Payment information

Contains debit-side information, such as the payment execution date, the originator's name, account details, and payment method. This section sets the foundation for the transaction batch.

3. Credit transfer transaction information

Focuses on individual transactions, detailing the credit side. This includes the payment reference, amount, currency, beneficiary information, regulatory requirements, and the purpose of the payment.

This organized structure ensures clear, consistent, and efficient data exchange across financial systems.

Transitioning to ISO 20022 may seem like a heavy lift for small community banks, but with the right approach, the migration can be manageable, cost-effective, and an opportunity to modernize operations. Below is a streamlined roadmap tailored for smaller financial institutions, with additional considerations for larger, more complex organizations.

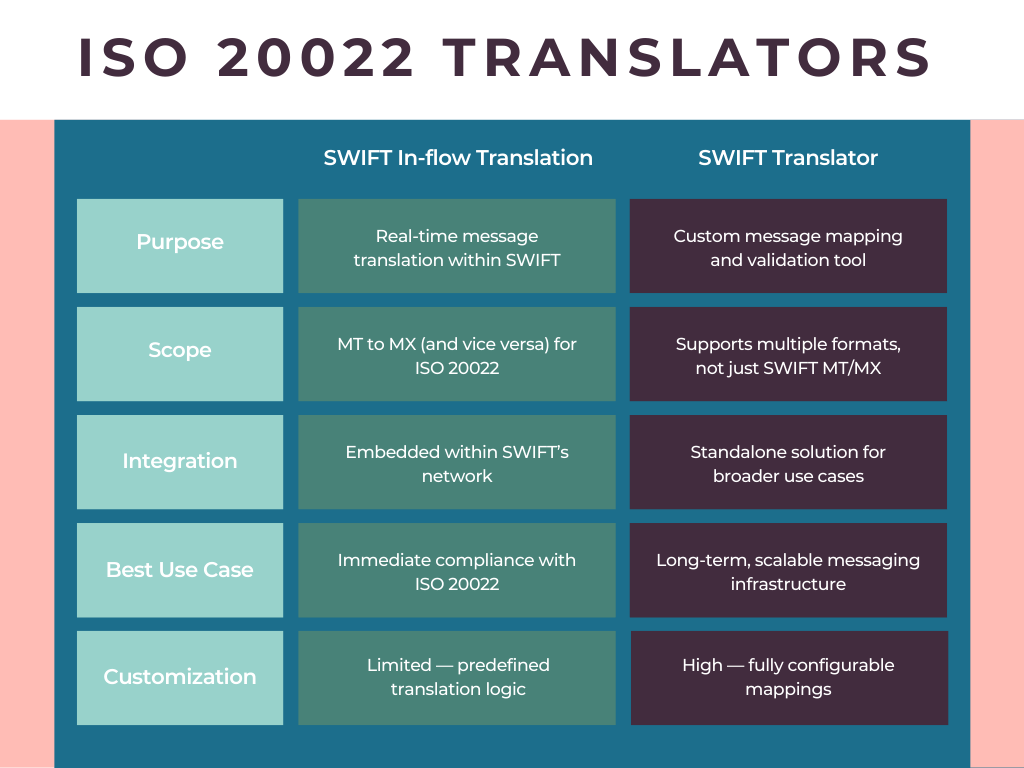

For most community banks, the transition to ISO 20022 will primarily involve translating older message formats (MT) into the new ISO 20022 format (MX). The good news is that this doesn’t require a complete system overhaul. Technology solutions, known as translation services, can bridge the gap between legacy systems and ISO 20022. These services automatically convert MT messages into ISO 20022 messages (and vice versa), allowing banks to meet compliance requirements without major changes to their existing infrastructure. Notable translation solutions include Swift's In-flow Translation service, which automatically converts messages during exchange, and Swift Translator, a standalone tool for defining, validating, and translating various message formats. In-flow Translation is a simpler, quick-fix solution for compliance, while SWIFT Translator is a more robust, customizable tool for institutions with complex messaging needs or long-term goals. Depending on the bank's strategy — whether it’s short-term compliance or investing in scalable solutions — either tool could be a fit.

Small banks don’t need to tackle ISO 20022 all at once. A phased approach may work best, according to SWIFT:

Start with high-priority payment types that require compliance, like cross-border wires.

Pilot the new message format for a small subset of transactions to ensure everything runs smoothly.

Gradually expand adoption to other areas as your team grows comfortable with the new system.

This incremental strategy helps reduce risk, ensures operational continuity, and allows time for staff training.

Community banks don’t need to reinvent the wheel. Trusted core providers offer affordable solutions tailored to small banks. These providers handle much of the technical heavy lifting, including:

Translating messages into ISO 20022 format.

Testing your systems to ensure compliance.

Mapping out a plan for future updates.

Consultants with ISO 20022 expertise are also valuable resources and can recommend translation services and third-party vendors that will work best for your financial institution.

As Klingensmith notes, “Many banks assume their system providers have it covered, but there’s a lot of downstream impact. A consultant can help you identify where rich data fields may not be mapped to your local systems, ensuring you’re fully compliant and prepared.”

For larger banks and credit unions, the transition may involve managing more sophisticated systems with multiple messaging formats and legacy platforms. These organizations often use Enterprise Application Integration (EAI) software, which acts as middleware to connect disparate systems and ensure smooth communication. EAI tools can:

Translate proprietary formats into ISO 20022 messages.

Enrich messages by pulling additional data from internal systems.

Streamline workflows across complex infrastructures.

This approach allows larger institutions to insulate their core systems from the complexities of ISO 20022, reuse existing functionality, and reduce overall implementation costs. For example, a bank operating in multiple regions can use EAI software to address region-specific ISO 20022 requirements, such as SEPA in Europe or FedWire in the U.S., while maintaining a consistent operational framework.

The cost of implementing ISO 20022 varies, but for community banks, the primary expenses will likely involve:

Translation services: Affordable tools that handle the conversion of messages between MT and ISO 20022 formats.

Testing and compliance: Ensuring systems are configured correctly to meet compliance deadlines.

Staff training: Help your team understand how the new system works and how to make the most of its features.

For larger institutions, costs may also include integrating EAI software or building native ISO 20022 capabilities. However, the investment pays off over time, as these systems enable greater efficiency, reduce manual intervention, and improve compliance processes.

By starting with basic translation tools, taking a phased approach, and partnering with experienced providers, community banks can achieve ISO 20022 compliance with minimal disruption. Meanwhile, larger institutions can leverage more advanced solutions like EAI to future-proof their operations and streamline complex workflows.

The road to ISO 20022 compliance isn’t without challenges. Legacy systems may need significant upgrades, and staff must be trained to handle new messaging formats. However, incremental upgrades focused on key message types can ease the transition. Additionally, educating clients about ISO 20022’s benefits — such as reduced fraud and faster payments — can help build trust and drive adoption.

The first step in ISO 20022 adoption is conducting a thorough assessment of your current systems to identify gaps. From there, you may want to work with third-party consultants to simulate transactions, test data flow, and validate integrations. Begin with a phased rollout, starting with high-priority payment types, and gradually expand your ISO 20022 capabilities. Acceleron, which builds community banking software for international wire processing, is actively implementing ISO 20022 on its platform, with CEO Damon Magnuski emphasizing the critical role of thorough testing in ensuring a smooth transition.

By acting now, community banks and credit unions can not only meet the November 2025 deadline but also position themselves as innovators in the financial industry. As Klingensmith puts it, “This isn’t just compliance — it’s a transformative opportunity for the industry to move forward together.”

At Acceleron, we are fully committed to our platform's compliance with ISO 20022 ahead of the November 2025 deadline. Our digital wire platform, which features a foreign exchange marketplace and currency conversion tool, is already well on its way.

“We're taking a proactive approach to implementing ISO 20022 by working with key vendors and adapting to new requirements as they emerge," says Acceleron Chief Technology Officer Kevin Minard.

"For example, we're reworking our message formats to comply with the pacs.008 standard (Financial Institution to Financial Institution Customer Credit Transfer), supporting additional fields like the UETR (Unique End-to-End Transaction Reference), which improves tracking and transparency for wire transfers," he says.

In preparation for the transition, Acceleron is implementing tools to validate and test message formats, as well as ensuring compatibility with all major user interfaces and foreign exchange providers. “We work with the major user interfaces that our clients use every single day," explains Damon Magnuski, CEO of Acceleron.

This readiness strategy involves continuous communication with vendors to align on evolving standards and avoid disruptions. "We’re staying ahead of potential conflicts by actively engaging with user interfaces and FX providers, ensuring we’re more compliant than required," adds Magnuski.

"Our clients can rest assured that whether it’s sending a payment to an FX provider or pushing data to a financial institution, everything will be ISO compliant and function seamlessly.”

With this approach, Acceleron is not only prepared to comply but also positioned to leverage ISO 20022 to deliver cleaner, more structured data that reduces errors, improves transparency, and supports compliance for financial institutions.

ISO 20022 evolves over time, with updates that address new regulatory and operational needs. Community banks should plan to keep their systems aligned with these updates to avoid compliance risks and take advantage of new opportunities, like enhanced fraud detection or better data insights. Your technology provider can typically handle these updates for you, so make sure to choose one with a strong track record of staying current with industry standards. We will be monitoring new developments as the deadline gets closer — stay tuned for latest updates on the Acceleron blog.